Be Aware of the Bird-Dog | Insurance & the Public Adjuster

“My best friend is a public adjuster,” said the roofer to the homeowner in the wake of wicked winds which whipped South Florida.

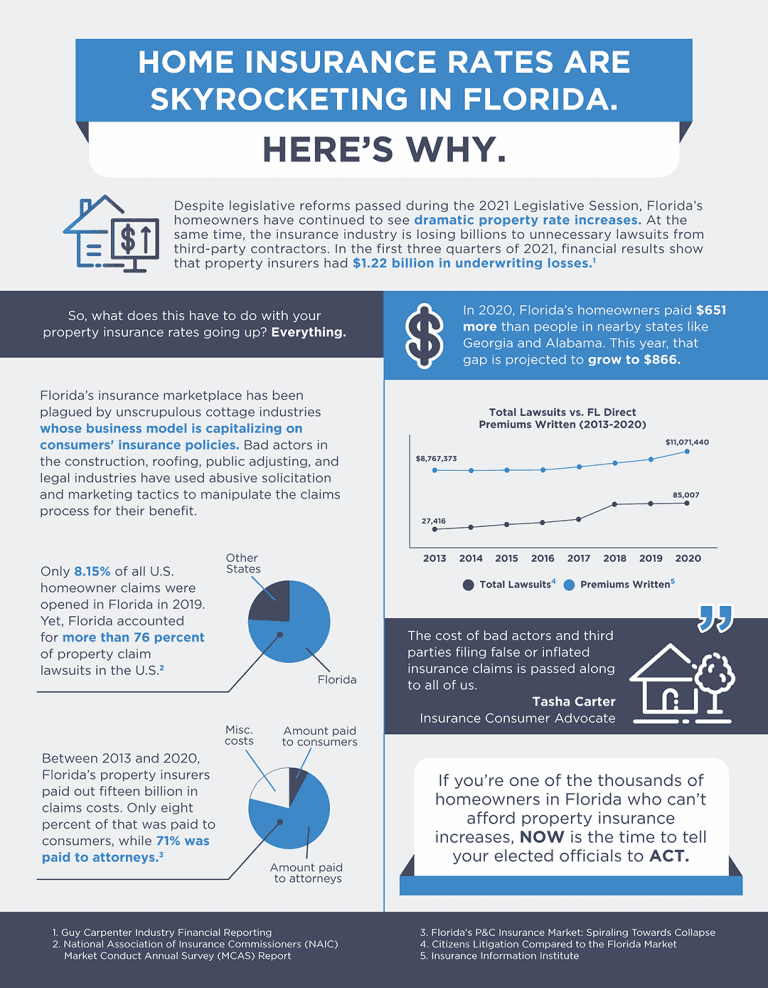

This scene is the opening act of a scam which has played out over and over again, costing us all money in the form of higher premiums. The first responder for repairs in the wake of a loss can influence an unsuspecting property owner who has no experience in dealing with these types of circumstances. When a roof is damaged by wind and the threat of a roof leak becomes real, getting someone who can deal with diagnosing the scope and extent of the damage and present a credible estimate of repair with the ability to complete the job on time and honor a warranty is highly sought after. If someone says they have a friend who is a public adjuster that can stick it to the insurance companies and get more money for the repairs than they actually cost so that the deducible can be covered without the insured having to lay out the money, then this is a red flag to any property owner in terms of the ethics of the individual who suggests such a thing. The principle of insurance is to be made whole after the loss.

In terms of property insurance, a specific amount of coverage is purchased to replace or repair a building or property subject to a deductible.

The reason for this is to avoid the moral hazard. In other words, insurance is based on people having a vested interest in maintaining their properties and, in return for a premium, an insurer provides indemnification for any unforeseen covered loss that may occur in the future subject to the limits shown on the policy as well as being subject to any deducible. The theory is that if there is a deductible, insureds will be more likely to maintain and mitigate potential loss because they have some skin in the game. A perversion of this concept is the use of an unscrupulous public adjuster who lures traumatized people at the moment of an emergency to sign over their insurance benefits in return for immediate repairs and possibly little or no deductible and is corrupt, in my opinion, since the repairs are often over-billed with questionable or shoddy workmanship which leaves most victims feeling deceived.

Don’t be a victim.

In the event of a loss, take immediate action to keep further damage from happening and document with photographs and receipts to evidence the steps taken to secure the property. Call your agent and/or insurer as soon as reasonably possible. This is of particular importance with regard to water damage, since there is generally a contractual responsibility on the part of the insured to notify the insurer of a loss within 14 days of noticing damage for the first time. The insurer’s intent is to respond with an adjuster in order to take the facts and document the occurrence while dispatching a field person to go and visually inspect and report on the actual damage. This information is viewed by a claims examiner who has access to data in order to calculate the dollar value of the damage and offer settlements once a final number is agreed upon.

A public adjuster may often inflate the damage in order to come back with a higher bill when in reality the actual cost of fixing the damage will be much more limited, producing a windfall to the insured. Insurers have been forced to litigate and in some cases pay inflated prices to avoid costly court action. When the premiums of the many pay for the claims of a few, but the claims are frequent and inflated, then everyone in the area suffers as a result in the form of higher premiums. Take action by being aware and know that there ain’t no free lunch.